IPD has started an interesting

new index in the French market, called the IPD Green Real estate index. It

basically analyses the performance of Green buildings and compares it with both

recent non-green buildings as well as with the general IPD index (http://aox.ag/KdpWzJ)

As far as I know, this is the

first time such an indicator is put together. This is more than welcome

initiative as it might once and for all stop the rhetorical debate about whether

or not Green adds value to the asset.

On the face of it, it looks as if

it does add value. Total return last year for the green building stood at 7,4%.

That is 1,1% higher than equivalent non green building which showed a total

return of 6,3%. However devil is in the details.

Here is how this performance is

broken up:

The green building performance is

solely driven by a (theoretical?) capital value improvement. It relative

performance is very poor in turns of Income Returns with assets yielding around

2% less than the rest of the market. More interestingly the IPD data reveal that

there is no rent difference between Green and non-green buildings (average ERV

is at 356 EUR/sqm/year for non-green vs 361 EUR/sqm/year for green building).

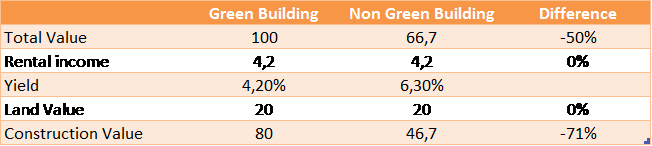

These data allow for an interesting

(theoretical) analysis about the benefit of investing in the green building. Let’s

assume a green office building which is worth 100. According to IPD data, this

asset will generate around 4,2 of rent. Let’s now assume a non-green building

asset generating the same rent. According to IPD this asset is yield 6,3% ie.

is worth 66,7. From there you can derive the actual value as described in the

following table.

As a result of the IPD data, you

can determine in a few minutes that the market offers a 71% premium for the

value of a “Green” construction over a non-green construction. At this stage it become clear what you want to build if you are a developper. The only economical explanation for such a premium would be that a green building will depreciate much slower than a non-green

building. It would therefore deserve a premium as it would deliver returns on a longuer period of time.

The table below, summarizes the

number of years needed to collect enough rent in order to pay for the

construction cost at a given unlevered expected return (the NPV of the cash

flow is equal to zero).

What the previous table show is that If you expect a 5% return from a non green building, assumes no terminal value, no rental growth, no capex... you need to collect the rent for 16 full years. For a green building for which a 71% premium was paid, you need to collect rent for 54 years. Another way to say this is that the premium reflect the belief that the green building life will be 3,3 times longuer than the non green building.

So now, here is the question:

Which assets do you think is going to generate the most sustainable returns

over time? I am not going to take position. However I have lost faith long ago

in Hal Jordan and the believe that “Green is the color of will”