IPD has started an interesting

new index in the French market, called the IPD Green Real estate index. It

basically analyses the performance of Green buildings and compares it with both

recent non-green buildings as well as with the general IPD index (http://aox.ag/KdpWzJ)

As far as I know, this is the

first time such an indicator is put together. This is more than welcome

initiative as it might once and for all stop the rhetorical debate about whether

or not Green adds value to the asset.

On the face of it, it looks as if

it does add value. Total return last year for the green building stood at 7,4%.

That is 1,1% higher than equivalent non green building which showed a total

return of 6,3%. However devil is in the details.

Here is how this performance is

broken up:

The green building performance is

solely driven by a (theoretical?) capital value improvement. It relative

performance is very poor in turns of Income Returns with assets yielding around

2% less than the rest of the market. More interestingly the IPD data reveal that

there is no rent difference between Green and non-green buildings (average ERV

is at 356 EUR/sqm/year for non-green vs 361 EUR/sqm/year for green building).

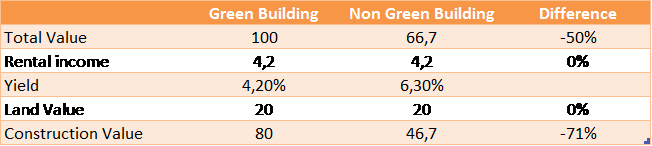

These data allow for an interesting

(theoretical) analysis about the benefit of investing in the green building. Let’s

assume a green office building which is worth 100. According to IPD data, this

asset will generate around 4,2 of rent. Let’s now assume a non-green building

asset generating the same rent. According to IPD this asset is yield 6,3% ie.

is worth 66,7. From there you can derive the actual value as described in the

following table.

As a result of the IPD data, you

can determine in a few minutes that the market offers a 71% premium for the

value of a “Green” construction over a non-green construction. At this stage it become clear what you want to build if you are a developper. The only economical explanation for such a premium would be that a green building will depreciate much slower than a non-green

building. It would therefore deserve a premium as it would deliver returns on a longuer period of time.

The table below, summarizes the

number of years needed to collect enough rent in order to pay for the

construction cost at a given unlevered expected return (the NPV of the cash

flow is equal to zero).

What the previous table show is that If you expect a 5% return from a non green building, assumes no terminal value, no rental growth, no capex... you need to collect the rent for 16 full years. For a green building for which a 71% premium was paid, you need to collect rent for 54 years. Another way to say this is that the premium reflect the belief that the green building life will be 3,3 times longuer than the non green building.

So now, here is the question:

Which assets do you think is going to generate the most sustainable returns

over time? I am not going to take position. However I have lost faith long ago

in Hal Jordan and the believe that “Green is the color of will”

The IPD France Green Building Indicator is the 3rd attempt from IPD to produce a financial performance index of "green" properties.

ReplyDeleteOur first is the IPD UK Sustainable Property Indicator (ISPI UK) which has never firmly concluded a performance differential for green and non-green properties.

In Australia, we have the IPD Australia Quarterly Green Property Index which clearly shows the link that better rated Green Star / NABERS Energy rated buildings financially out perform lower / unrated properties.

The IPD France Green Building Indicator has just been released for the second time. It shows some performance differential, but the sample sizes are small and the history is short. So, we release the results for market transparency but we do not draw any conclusions that in France green buildings out perform financially.

IPD indices are valuation-based indices and until the valuers are taking environmental considerations into account in their regular appraisal process (as they are in Australia), any performance differential cannot be put down to environmental reasons.

For more information, go to www.ipd.com/ispi.

Christina Cudworth

Global Head of Sustainability, IPD

Mr. Elaminé, very interesting original post, very convincing reasoning.

ReplyDeleteI was just wondering whether the unknown variable that could explain the surprising value differential might be something more down-to-earth than the "environmental considerations" that Ms. Cudworth is mentioning:

Heatings costs.

They will hopefully be lower for the "green" style building.

Therefore, for a given rent (which should usually exclude the heating costs), a tenant would have to bear less heating costs than for a conventional building.

Put differently: For a given quantity of sqm with same location and therefore same gross rent (including heating), the green building should yield a higher net rent (excluding heating). Of course the building costs are higher per sqm and therefore if this effect is proportionally higher than the net rent increase, the yield on the construction in % is lower.

The only reason for an "equilibrium" market price for green buildings with a lower current rent yield in % I can find would be future increases in heating costs. E.g. if heating costs would increase by say 5% p.a., (net) rents for green buildings could increase more than for conventional buildings (maybe not in one given contract, but certainly with a new tenant).

What numbers of heating cost increase would be needed to justify such a gap in current yield is an interesting question, as I don't have a feeling of how much heating costs for offices are in comparison to total rent, I would rather not try to fill in an example here...

With best regards,

Gerrit Roth

PS: Sorry if I might not have used the right expressions for the "gross" and "net" rent (Warm- und Kaltmiete).